Overview

A self-managed superannuation fund (SMSF), also known as Superannuation Trust, is established for the sole purpose of providing benefits to the members of the fund in retirement. The SMSF Trustee can be either individuals, who are also the members of the fund or a company, also called corporate trustee whose directors are members of the SMSF. The SMSF is structured in the way that makes sure the investment decisions and implementation of the strategy of the fund are controlled by the members and for the benefit of the members.

An SMSF is highly regulated and often requires the assistance of SMSF specialists to ensure ongoing compliance. A Patricia Holdings SMSF Deed is drafted by a Trust Law specialist and is drafted to comply with the current legislation to ensure the fund is established properly.

We make setting up an SMSF easy with a few simple steps. You can now set up a SMSF online and receive your tailored SMSF trust deed in less than 15 minutes.

If you set up an SMSF with a corporate trustee, our SMSF package is the best time-saving option for you.

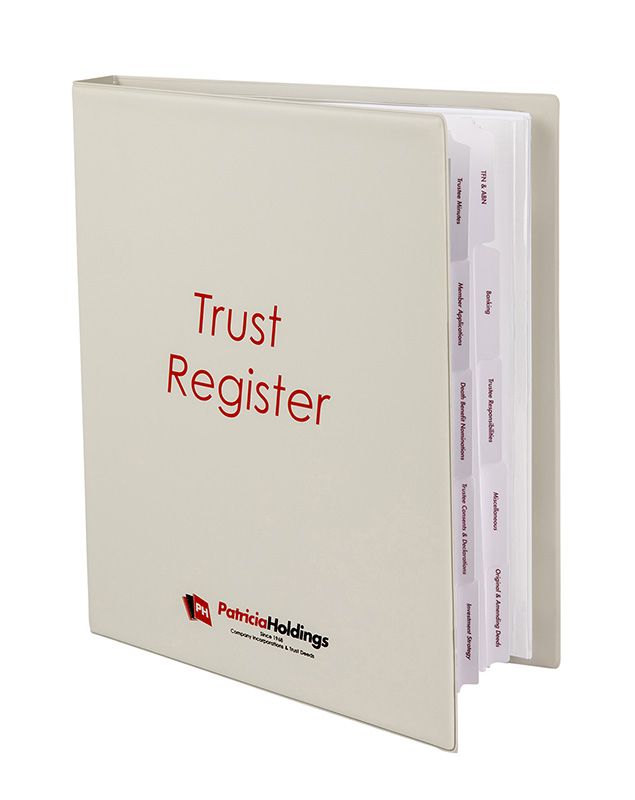

You can either order a PDF copy of the SMSF Trust Deed or a full-service courier product in which you will receive your documents bound in a professional folder which includes indexed tabs separating the documents and 3 copies of your SMSF Trust Deed (2 bound and 1 hole punched).

After the SMSF trust is established, we can also help with ABN application for the trust.

What is included?

{kind=link}

- A4 binder

- 2 bound copies of the SMSF trust deed

- 1 hole punched copy of trust deed

- Dividers

- Instruction sheet

- Notes for the assistance of the Trustee

- Product Disclosure Statement

- Minutes to set up the SMSF

- Suggested Investment Strategy

- Request to open a bank account for the SMSF

- Certificate of Compliance

- Application for Membership

- Consents for the Trustees, or directors of the corporate Trustee

- Binding Death Benefit Nomination form

Pricing

| Online (incl gst) | Email (incl gst) | |

|---|---|---|

PDF email delivery

|

$242 |

$352 |

Full Service Courier delivery

|

$352 |

$462 |

Optional Extras

|

Delivery Information

For email delivery orders ordered online, the Trust Deed and related documentation will be emailed to you within 15 minutes of placing your order. If you have ordered an SMSF and Trustee company package, we need to register the company before establishing the Trust which means delivery may take up to 90 minutes for both the company register and the Trust deed.

We are able to deliver our full service couriered product to the Sydney metropolitan area within about 5 hours of receiving an order. Orders received before 12 midday are usually delivered the same day. Documents being sent to Brisbane and Melbourne will be sent by courier or express post and are often delivered the next day (orders must be received by 1pm for delivery the next day) and within a couple of days to Perth and regional areas.

Trust FAQs

What is a Self-Managed Superannuation Fund (SMSF)?

A Self-Managed Superannuation Fund (SMSF) is a Superannuation Trust.

An SMSF is a trust structure that provides benefits to its Members upon retirement. The main difference between an SMSF and other super funds is that the Members are also the Trustees of the fund giving them a high level of control when it comes to tailoring the fund to meet their individual needs.

What are the conditions of a SMSF according to the Superannuation Industry (Supervision) Act (SIS Act)?

- SMSFs must have 6 or fewer members.

- The Trustee(s) will either be individuals who are all members of the SMSF, or a Corporate Trustee whereby all Directors are members of the SMSF.

- If there is only one member of the fund then that member plus another person unrelated to the Member will be Trustees.

- No member can be an employee of another member - unless the two members are related.

- For a single Member SMSF with a Corporate Trustee, either the single Member will be the Sole Director of the company or it will be a company with two directors whereby the second Director is a relative of the member only if they are the employer of the Member or a non-relative of the member if they are not their employer.

- No trustee can receive payment from the fund for their services as trustee.

How is a binding death benefit nomination updated?

The Patricia Holdings Trust deed provides that the Nominations can be renewed every 3 years but do not have to be renewed. It also provides that there can be an agreement between the Trustee and the Members (that binds the Trustee) setting out how the members benefits are to be distributed if the member dies.

When should a SMSF trust deed be updated?

A Superannuation Trust deed should be updated whenever there is a significant change in the law. As a general rule of thumb the Trustees of a Superannuation Fund should consider reviewing the Trust deed every two years and should update at least every four years. The Funds Auditor may provide some guidance regarding this.

How is the name of a Superannuation Fund changed?

Patricia Holdings can help change the name of your SMSF. The Trustee elects to change the name of the Fund and then confirms that election in writing. A Trustee must ensure that if a Fund changes its name that every person who has business dealings with the Fund and every Nominated Beneficiary of the Fund are notified of the change of name. We can provide services for SMSF changes, with all the required paperwork for $187 delivered as a PDF or $220 for printed and couriered documents.

Does a SMSF have to have a Trustee?

Yes, every SMSF must have a Trustee. This is because the law requires that for a Trust (an SMSF is a Trust) to exist there must firstly be some Trust property and secondly, it is the Trustee (or Trustees) who hold the Trust property on Trust for a Beneficiary or Beneficiaries (there must be a separation between the legal and equitable ownership). A Trust is not considered a legal entity.

In the case of Superannuation Trust the Superannuation Laws requires that a Superannuation Trust must have a Trustee.

All the SMSF Members must be Trustees if the Trustees are individuals (except in the case of Members who are not eligible to be Trustees i.e. minors, bankrupt, unsound mind, then an authorised representative would be appointed) and if the Trustee is a company then all of the Members must be the directors of the Trustee Company where eligible.

If there is only one member then there must be 2 Trustees if the Trustees are individuals. The Trustee who is not the member can be a relative of the member only if they are the employer of the Member or a non-relative of the member if they are not their employer.

If there is only one member and the Trustee is a company then the Trustee company can be a single member company of which the member is the sole director or it can be a two Director company whereby the second Director is a relative of the member only if they are the employer of the Member or a non-relative of the member if they are not their employer.

How is a SMSF wound up?

A Trustee winds up a Superannuation Trust by:

- making a Declaration (in writing) that the SMSF is to vest (that is the Trust ends and the Trust assets be distributed to the Beneficiaries);

- collecting in all of the Trust assets and converting them into cash (unless the Trustee proposes to make an in specie distribution);

- all debts of the SMSF must be paid and all tax must be paid;

- The assets (or cash) are then distributed amongst the Members or Members dependants according to the members share in the SMSF;

- notice is then given to the Taxation Department that the Trust has ceased to exist.

If any Member is under the age (retirement after age 55, permanent disability, death etc) when the Superannuation Trust can make payments to the Member then that particular Members share must be paid to another complying Superannuation Fund.

Who can be a Trustee of a SMSF Trust deed?

Under section 17 of the SIS Act (and as set out in the definitions section of the Patricia Holdings SMSF Trust deed) the Members must be the Trustees, or if the Trustee is a Company then the Directors of the Trustee Company must be the same persons as the members.

If there is only one Member of the Superannuation Fund then that Member plus another person unrelated to the Member will be Trustees, unless that second person is the employer of the member then they should be related. For a single Member SMSF with a Corporate Trustee, either the single Member will be the Sole Director of the Company or it will be a two Director company with the Member being one and an unrelated second person being the other (unless they are the employee of the Member as above).

Minors (a person under 18) cannot be Trustees or Directors of a Trustee Company. But a Legal Personal Representative of a minor can represent the minor.

Bankrupted and disqualified persons cannot be Trustees' or Directors of a Trustee Company.

Can SMSF’s members be non-Australian residents?

Yes, members of the fund can be non-Australian residents. However, if all members of the SMSF live overseas for an extended period, it could result in significant tax implications.

Can a member be under a "legal disability" and still be a member?

Yes, a member can be considered to have a "legal disability" (excluding being under 18), provided that the legal personal representative of the disabled member is a trustee of the fund, or if the member lacks a legal personal representative, a parent or guardian of the disabled member acts as a trustee.

If the trustee is a company, the legal personal representative of the disabled member, or in the absence of one, a parent or guardian of the disabled member, must serve as a director of the company in place of the member.

How and when can payments be made from my SMSF to its Members?

You can access your super when you reach your preservation age. This is the minimum age, set by law, which your super must be preserved until and is currently between 55 and 60. Once you reach this age, you can access your super as long as you are permanently retired (or reached age 65). If you haven’t permanently retired, you can still access part of your super through a transition to retirement pension.

When the Trustees of the Superannuation Fund are individuals then payments from the SMSF to its Members must be made in the form of a pension. That restriction does not apply in the case of a Corporate Trustee. In this instance, payments can be made in lump sum or pension.

Does the SMSF have to apply for an ABN?

Yes, the SMSF will receive an ABN when it registers with the ATO and elects to become a regulated superannuation fund. Patricia Holdings can help with the fund's ABN, TFN, and GST registrations.

To obtain an ABN, the fund must meet the following requirements:

- Have at least one trustee

- Have a trust deed

- Have identifiable members

- Set aside assets for the benefit of its members

Can the Trustee of a Bare Trust used for Limited Recourse Borrowing Arrangements be the same as the Trustee of the related Superannuation Trust?

If the trustee is a corporate trustee then the answer is no. The Superannuation Industry Supervision Act is specific, under section 67 A & B that the Trustee must be a different legal entity. The Trustee can be an individual, a group of individuals or a Company. Directors of the Corporate Trustee of the Bare Trust can be the same as the members of the Fund.

It is in our experience that most banks will not lend to a Bare Trust with individual Trustees.

What happens when all of the Members of a SMSF have died?

When all of the Members of an SMSF have died the assets of the SMSF must be distributed amongst the dependants of the deceased Members or paid to the personal legal representative of the deceased Members to be distributed in accordance with the Will of the deceased Members. If a SMSF Member has given the Trustee a direction in writing either in the form of a binding death benefit nomination or in some other form then the Trustee may distribute the Member's share of the fund in accordance with that direction.

Care should be taken when distributing a deceased Member's share of a SMSF because there are different taxation consequences attached to different distributions.

Can death benefit nominations be non-binding?

Yes, the law was changed in 2008 to allow non-binding death benefit nominations, and these are permitted by the Patricia Holdings deed. A Death Benefit Nomination form will be provided with any deed purchase.